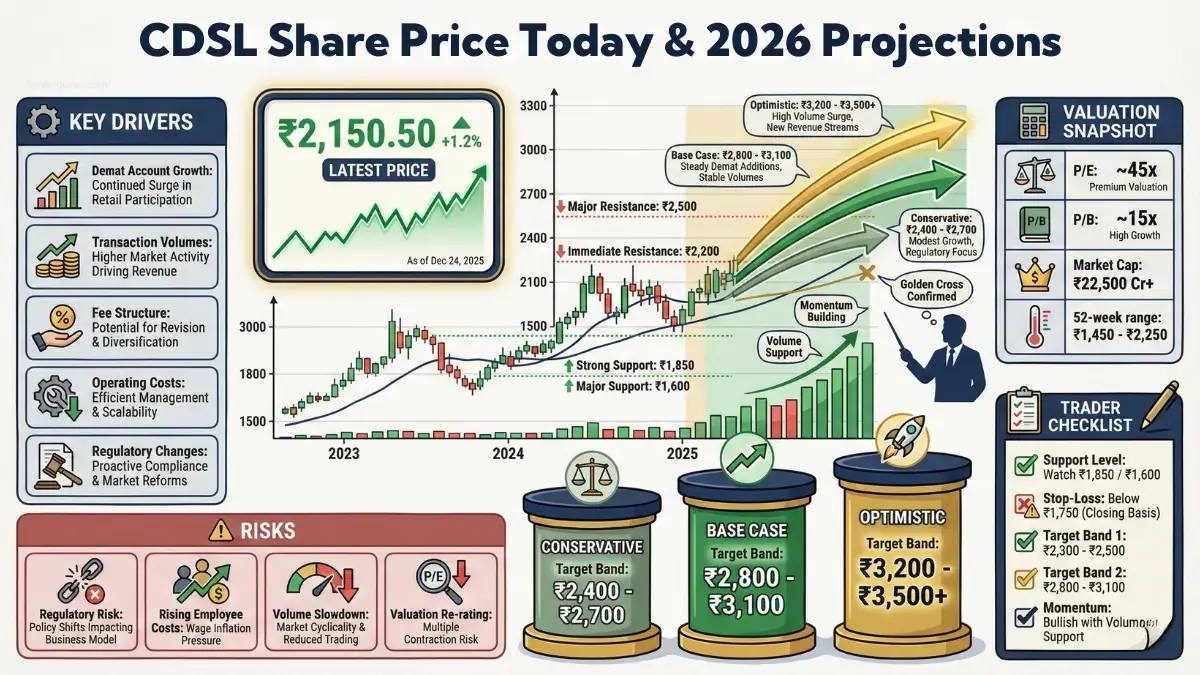

Central Depository Services (India) Ltd (Organization) commands a dominant position in the Indian capital markets. The date reads December 24, 2025. Investors monitor the ticker closely. The stock reflects the broader health of the Indian financial ecosystem. This analysis provides a deep dive into valuation, operational metrics, and price targets. We examine the numbers. We scrutinize the growth drivers. We evaluate the risks. You receive actionable data to inform your portfolio decisions.

The Strategic Position of CDSL in 2025

CDSL functions as the backbone of the Indian securities market. The company holds securities in electronic form. This service enables book-entry transfer of securities. The business model relies on volume. More investors mean more revenue. The Indian market witnessed a massive surge in retail participation between 2020 and 2025. CDSL benefited directly from this trend.

The company operates as a Market Infrastructure Institution (MII). This status grants stability. Barriers to entry remain high. Regulatory hurdles prevent new competitors from easily entering the space. CDSL shares the market with NSDL. This duopoly structure ensures pricing power and consistent margins. The company does not need to spend heavily on marketing. The customers come to them. Depository participants (DPs) open accounts. CDSL collects the annual maintenance charges and transaction fees.

Revenue Streams Breakdown

Understanding the stock requires understanding the income sources. CDSL generates cash through multiple channels:

Annual Issuer Charges: Companies listed on exchanges pay fees to CDSL. As more companies launch IPOs, this revenue stream grows. The IPO boom of 2024 and 2025 added significant recurring revenue.

Transaction Charges: Every time an investor sells shares, a fee applies. High market volatility benefits CDSL. High trading volume translates to higher earnings.

Online Data Charges: The KYC registration agency (KRA) business contributes to the top line. Verification services remain mandatory. CDSL monetizes this requirement.

Corporate Action Fees: Dividends, splits, and bonuses trigger corporate action events. CDSL charges for processing these events.

Scenario table — targets, drivers, and trade implications

Scenario | Target (late‑2025 / near‑term) | Primary driver | Trade implication |

|---|---|---|---|

Conservative | ₹1,400–₹1,600 | Slower account growth; margin pressure | Defensive; wait for earnings recovery |

Base Case | ₹1,650–₹1,900 | Stable demat growth; cost control | Accumulate on dips with 6–12m horizon |

Optimistic | ₹2,000+ | Strong fee expansion; regulatory tailwinds | Add on breakout above ₹1,900 with volume confirmation |

Sources: Moneymintidea.com

Financial Health Check: December 2025

The financial statements for the quarter ending September 2025 reveal a robust balance sheet. The company maintains zero debt. Cash reserves continue to pile up. The operating margins consistently stay above 50%. This efficiency makes the stock attractive during uncertain economic times. Low fixed costs allow profits to scale faster than revenue.

Net profit growth has tracked the rise in demat accounts. The total number of active demat accounts in India crossed significant milestones earlier this year. CDSL manages the majority of these accounts. The focus on low-cost services attracted discount brokers. These brokers brought in millions of retail clients. CDSL serves as the preferred depository for these high-growth entities.

Return on Equity (ROE) and Return on Capital Employed (ROCE) figures remain impressive. These metrics highlight management efficiency. The company reinvests capital effectively. Shareholders receive rewards through regular dividends. The dividend yield offers a cushion against minor price corrections.

The Moat: Why CDSL Dominates

Warren Buffett often speaks of a "moat." CDSL possesses a wide one. The switching costs for a depository participant (DP) are high. Moving millions of accounts from one depository to another creates logistical nightmares. Therefore, DPs stay put. This retention creates a sticky revenue base.

Network effects also play a role. As more DPs join CDSL, the value of the network increases. The integration with stock exchanges and clearing corporations creates a seamless ecosystem. Any new entrant would struggle to replicate this infrastructure. The regulatory approval process alone takes years. CDSL sits securely within this fortress.

The cost advantage helps as well. CDSL traditionally kept charges lower than the competition. This strategy won the volume war. Volume leadership matters in a platform business. The marginal cost of adding one new account approaches zero. The revenue from the account flows almost entirely to the bottom line.

Market Drivers for 2026 and Beyond

Investors must look forward. Several factors will dictate the price trajectory heading into 2026:

1. Continued Retail Expansion

India still has low stock market penetration compared to developed economies. The percentage of the population investing in equities continues to rise. Financial literacy programs show results. Tier 2 and Tier 3 cities drive the next wave of growth. CDSL benefits most from this demographic shift. These new investors open accounts primarily through discount brokers aligned with CDSL.

2. The IPO Pipeline

The primary market remains active. Dozens of companies plan listings for 2026. Each new listing adds to the annuity income for CDSL. The securities become dematerialized. The issuer pays annual fees. This compounding effect strengthens the long-term valuation.

3. Mutual Fund Growth

Systematic Investment Plans (SIPs) bring steady inflows. Mutual funds hold units in demat form. The growth of the mutual fund industry parallels the growth of CDSL. Asset management companies (AMCs) rely on depositories for unit holding and transfer.

4. Regulatory Tailwinds

SEBI continues to push for transparency and digitization. T+0 settlement cycles are now standard. Faster settlements require robust technology. CDSL invested early in tech infrastructure. This readiness positions the firm to handle increased velocity in trade settlements without service disruption.

Risks to the Bull Case

No investment comes without risk. You must consider the downsides.

Market Cyclicality: A prolonged bear market hurts transaction revenue. If investors stop trading, fee income drops. The annuity income (annual charges) remains, yet the growth rate slows.

Regulatory Pricing Caps: The regulator monitors fees. SEBI might intervene if charges become perceived as excessive. A cap on transaction charges would impact profitability immediately.

Cybersecurity Threats: CDSL holds sensitive financial data. A data breach represents a catastrophic risk. Trust defines the business. Loss of trust leads to loss of clients. The company spends heavily on security, yet the threat persists.

Technology Disruption: Blockchain technology offers a theoretical alternative to centralized depositories. While adoption takes time, decentralized finance (DeFi) presents a long-term existential question for traditional intermediaries.

Technical Chart Analysis

The price action on the charts tells a story of consolidation followed by expansion. We analyze the weekly and monthly timeframes.

Support Levels

Strong buyer interest appears at the 50-week moving average. Institutional investors accumulate shares during dips to this level. Psychological round numbers also act as floors. The price history shows strong demand zones established during previous correction phases. These zones serve as safety nets for long-term holders.

Resistance Levels

Previous all-time highs act as the primary ceiling. The stock often pauses at these levels to digest gains. Traders take profits here. Breaking through these resistance points usually requires high volume. Volume confirms the strength of the breakout. Watch the volume bars closely. Low volume breakouts often fail.

Momentum Indicators

The Relative Strength Index (RSI) on the monthly chart indicates the long-term trend strength. Overbought conditions do not necessarily mean a sell. In strong growth stocks, overbought conditions persist for extended periods. The MACD histogram shows the momentum direction. Currently, the trend favors the bulls, provided the broader market remains stable.

Future Price Targets: 2026-2030

We project price targets based on earnings growth estimates and valuation multiples. Please note these projections rely on current data trends.

2026 Outlook

Analysts expect earnings to grow by 15% to 20%. The Price-to-Earnings (P/E) ratio likely remains premium due to the monopoly characteristics.

Conservative Estimate: Moderate growth in demat accounts. Stable market conditions. Target implies a 10% upside from current levels.

Aggressive Estimate: Bull market continuation. Surge in IPOs. Target implies a 25% upside.

2027 Outlook

By 2027, the impact of newer financial products will materialize. Single stock futures and increased derivatives participation will drive volume.

- Target Range: The stock typically commands a high valuation multiple. Assuming earnings compound at 18%, the share price should reflect this growth. Investors should look for a doubling of earnings every four to five years.

2030 Long-Term View

The Indian economy aims for the $7 trillion mark or higher by 2030. The financial sector acts as a proxy for this growth. CDSL will likely handle a vast majority of the paperless assets.

- Strategic Goal: Long-term holders should focus on the compounding of dividends and capital appreciation. The stock fits well in a retirement portfolio. The defensive nature of the business protects capital, while the growth aspect builds wealth.

Institutional vs Retail Holdings

Shareholding patterns reveal smart money movements. Foreign Institutional Investors (FIIs) and Domestic Institutional Investors (DIIs) hold significant stakes.

FII Trends: Foreign funds prefer monopolies. They like the predictability of cash flows. FII ownership has shown stability. They do not sell aggressively during minor corrections.

DII Trends: Indian mutual funds continue to buy. They understand the domestic retail story better than anyone. High DII ownership signals confidence in the local market structure.

Retail Investors: Retail holding remains high. This creates volatility. Retail investors tend to panic sell during downturns. Contrarian investors use these panic moments to accumulate shares.

The Role of Technology and Insurance in Depository Services

CDSL Ventures Limited (CVL) is a wholly-owned subsidiary. CVL was the first KYC Registration Agency. This subsidiary diversifies revenue. CDSL also explores insurance repository services. Holding insurance policies in electronic form reduces paperwork and fraud.

The insurance sector in India grows rapidly. Digital issuance of policies becomes the norm. CDSL stands ready to capture this market. The digitization of academic records via the National Academic Depository (NAD) also falls under their purview. These initiatives show management's intent to diversify beyond just stocks.

Comparison with Global Peers

Comparing CDSL to global peers provides context on valuation. Depositories in developed markets often trade at lower multiples. However, those markets grow slowly. The Indian market offers high growth. This growth justifies the premium valuation.

US-based depositories focus on custody and settlement. Their revenue mix differs. They rely more on interest income from cash balances. CDSL relies more on transaction and account fees. The Indian model offers better leverage to market activity.

Emerging market peers in Brazil or China trade at similar multiples to CDSL. Investors pay for the demographic dividend. The sheer number of potential new investors in India supports the higher multiples.

Actionable Investment Strategy

You need a plan. Do not trade on emotion. Follow these steps based on the analysis.

1. The Accumulation Strategy: Do not buy the full position at once. Use a staggered approach. Allocate capital in tranches. Buy 30% now. Buy 30% on a 5% dip. Buy the final 40% on a 10% correction. This averages your cost.

2. The Stop-Loss Discipline: Traders must protect capital. Set a stop loss below key technical support levels. If the 200-day moving average breaks, exit the trade. Re-evaluate later. Long-term investors might ignore this, yet traders must adhere to it.

3. Monitoring Key Metrics: Watch the quarterly release of demat account addition numbers. This single metric correlates most tightly with the stock price. If account additions slow down for two consecutive quarters, review the thesis.

4. Dividend Reinvestment: The company pays dividends. Reinvest these payouts. Buying more shares with dividend income accelerates compounding. Over a ten-year horizon, this makes a massive difference.

Analysis of Recent Price Movements (Q4 2025)

The last three months showed volatility. The stock reacted to global interest rate decisions. The Federal Reserve and the RBI policy shifts impact liquidity. Liquidity drives equity markets.

When rates fall, equity valuations rise. The discount rate decreases. Future cash flows become more valuable. The market anticipates a softer interest rate regime heading into 2026. This expectation supports the current stock price.

Volume analysis reveals accumulation. The up-moves occur on higher volume than the down-moves. This pattern suggests that large players are buying the dip. They absorb the supply coming from weak hands.

Defense and Offense Blend

CDSL offers a unique blend of defense and offense. The defensive characteristics come from the annuity revenue and the monopoly status. The offensive characteristics come from the exposure to the Indian equity cult.

The company remains profitable. The balance sheet stays clean. The growth runway extends for years. Risks exist, primarily regulatory and cyclical. Yet, the reward potential outweighs the risks for a patient investor.

Investors looking for exposure to the financialization of savings in India find a strong candidate here. The stock allows you to bet on the growth of the market itself, rather than picking individual winning companies. If the Indian stock market grows, CDSL grows. The correlation remains undeniable.

Focus on the long term. Ignore the daily noise. The structural story remains intact. CDSL continues to facilitate the wealth creation journey for millions of Indians. The share price will likely reflect this value creation over time. Position your portfolio accordingly.

Key Takeaways

Duopoly Power: Limited competition ensures stable margins.

Zero Debt: Financial freedom allows for agility.

Recurring Revenue: Annual fees provide a safety net.

Growth Potential: India's low equity penetration offers a massive runway.

Valuation: Premium multiples justified by high growth rates.

Strategy: Buy on dips. Hold for the long cycle.

You should also read: https://www.tradingview.com/symbols/NSE-CDSL/forecast/, It is a complementary article.