Intel Core Ultra Series 3 Stock Price Impact 18

Wall Street rallies on 'sold out' server capacity and rumored Apple foundry wins for Panther Lake.

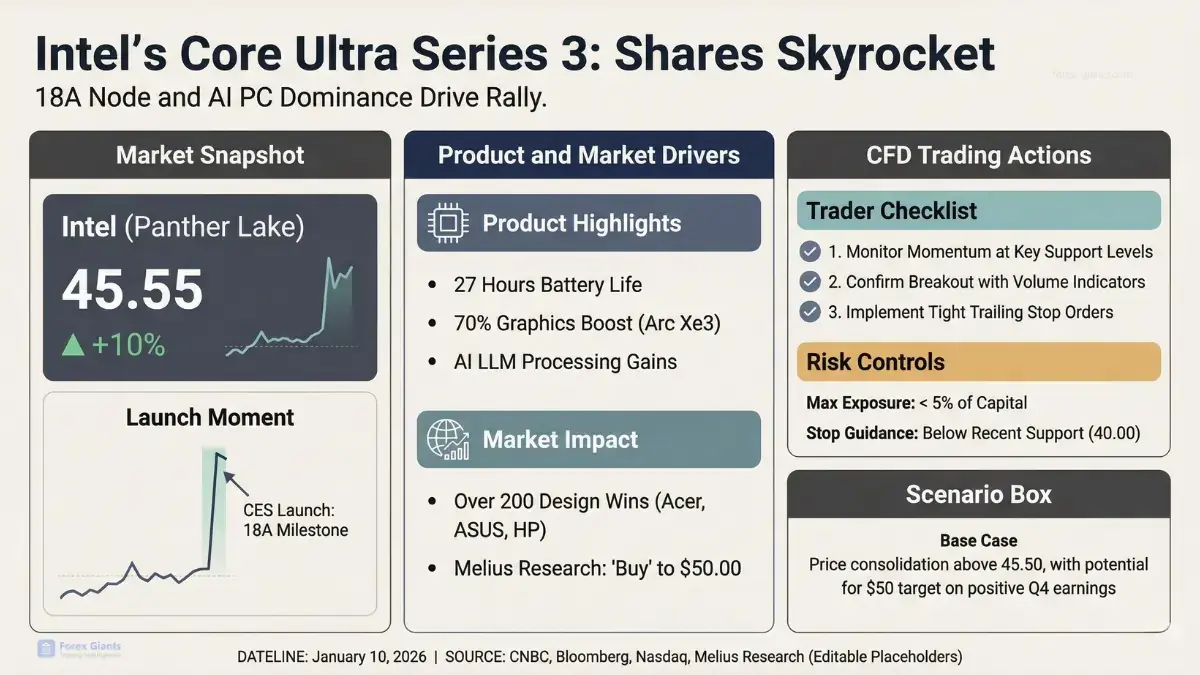

Intel (INTC) stock has surged near a 52-week high of $49 following the successful debut of the Core Ultra Series 3 'Panther Lake' processors. The rally is underscored by reports of a total capacity sell-out in the server division and a major strategic pivot to the 18A manufacturing node.

Market Catalyst: The 18A Inflection Point

Intel Corporation (NASDAQ: INTC) has entered a high-velocity recovery phase as of January 18, 2026, with shares climbing nearly 19% year-to-date following the launch of its Core Ultra Series 3 processors. The stock's performance, which saw a momentum-heavy close on Friday, is being driven by the successful deployment of the 18A (2-nanometer class) manufacturing process, which analysts describe as the company's most significant technological lead in a decade.

KeyBanc and Melius Research have recently upgraded the stock, with price targets shifting toward the $50-$60 range. This optimism stems from a combination of breakthrough consumer silicon and a historic turnaround in Intel’s foundry business.

Panther Lake: Benchmarking the Future

The Core Ultra Series 3, codenamed Panther Lake, has stunned the industry with performance metrics that directly challenge rivals AMD and Apple. Early benchmarks for the flagship Core Ultra X9 388H reveal:

Graphics: A 77% increase in gaming performance over the previous generation, powered by the new Xe3 architecture.

Efficiency: Over 27 hours of battery life in reference laptop designs, achieving parity with ARM-based competitors.

AI Compute: Integrated NPU capabilities that meet the latest requirements for "Next-Gen AI PCs," positioning Intel as the primary supplier for over 200 upcoming laptop designs from Acer, ASUS, and HP.

The 'Big Whale' Wins: Apple and Nvidia

Institutional sentiment shifted aggressively after reports surfaced of Intel securing "whale" customers for its Foundry Services. According to recent supply chain checks by KeyBanc, Intel has reportedly landed Apple as a customer for its 18A-P process to manufacture low-end chips for iPads and Macs.

Furthermore, the capital injection from Nvidia’s $5 billion co-development deal and a 10% equity stake taken by the U.S. Government have de-risked the balance sheet, allowing CEO Lip-Bu Tan to focus on aggressive production scaling. Analysts report that Intel's data center server CPUs are "almost sold out" for the remainder of 2026, a scenario that was unthinkable during the company's 2024 slump.

Analyst Perspective and Valuation

While the rally has been fierce, some analysts remain cautious regarding Intel’s forward P/E ratio, which has expanded to 77x. Jefferies recently raised its target to $45 but maintained a 'Hold,' citing potential supply constraints as Intel shifts capacity from legacy nodes to the high-demand 18A lines.

However, the prevailing consensus suggests that if Intel maintains its 18A execution through the Q1 2026 earnings report, the current 'skyrocket' in share price could be the floor for a long-term valuation rerating. Investors are now looking toward the January 22 earnings call for confirmation of gross margin improvements beyond the 36% threshold.

Jesus Guzman

Founder & Lead Analyst

Jesus is the founder of FN Pulse and a veteran trader with over 15 years of experience in financial markets. He specializes in quantitative analysis and is passionate about bringing transparency and data-driven insights to the retail trading industry.