Research Report: The AI Infrastructure Supercycle

Abstract

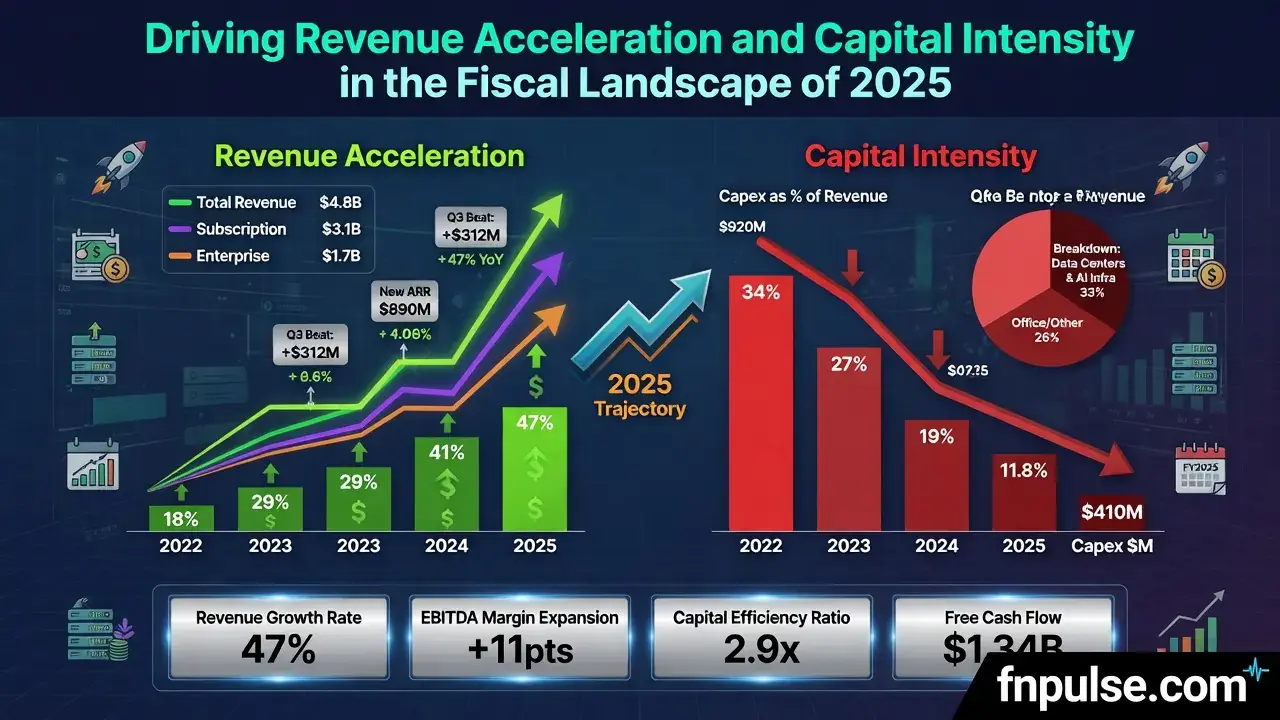

Driving Revenue Acceleration and Capital Intensity in the Fiscal Landscape of 2025

Full Research

Author: Jesus Guzman

Date: December 2025

Sector: Technology, Global Markets, Macroeconomics

1. Executive Summary

The fiscal landscape for the first half of 2025 reveals a distinct economic bifurcation: companies enabling the artificial intelligence (AI) and cloud infrastructure build-out are reporting accelerating revenues and expanding margins, while simultaneously committing to historic levels of capital expenditure (CapEx). Conversely, adopters in traditional sectors are beginning to realize operational efficiencies, using AI to protect margins against macroeconomic headwinds.

This report analyzes Q1-Q2 2025 financial disclosures from major global equities to determine how AI and cloud investments are reshaping corporate financial results. The data suggests we are in the investment phase of a new technological supercycle, characterized by a split between Infrastructure Builders (accretion via CapEx) and Enterprise Adopters (margin defense via efficiency).

2. Sector Analysis: The Infrastructure Builders

2.1. Cloud Hyperscalers: Accelerating Revenue and Operating Leverage

For the major cloud providers ("hyperscalers"), AI has transitioned from a theoretical growth driver to a primary revenue engine, reversing previous optimization trends.

Revenue Acceleration: Google Cloud reported a 32% year-over-year revenue increase in Q2 2025 to $13.6 billion, with an annual revenue run-rate surpassing $50 billion. Microsoft reported Intelligent Cloud revenue growth of 21% in fiscal Q3, with Azure surging 33%.1 AWS sales increased 17.5% YoY to $30.9 billion, citing "triple-digit" growth in AI businesses.2

Operating Margin Expansion: Despite heavy investment, cloud margins are expanding due to scale. Alphabet saw Google Cloud operating margins expand to 20.7% in Q2 2025 (up from 11.3% prior).3

Historic Capital Expenditures: CapEx is soaring to support this growth. Alphabet raised its 2025 outlook to ~$85 billion.4 Microsoft’s CapEx hit $24.2 billion in a single quarter (ended June 30, 2025).5 Meta narrowed its full-year forecast to $66−72 billion, citing urgent capacity needs for AI models.6

2.2. Semiconductors and Hardware: The "Pick and Shovel" Windfall

Upstream suppliers are recording some of the most dramatic financial expansions in corporate history.

Data Center Dominance: NVIDIA reported Q2 fiscal 2026 revenue of $46.7 billion (up 56% YoY), with Data Center revenue accounting for $41.1 billion.7

High-Performance Computing (HPC): TSMC reported that HPC now accounts for 60% of revenue, driving a 30% increase in full-year guidance.8

Memory Recovery: Samsung Electronics noted an 11% sequential sales rise in its semiconductor division, driven by High Bandwidth Memory (HBM) for AI servers.9

Networking Infrastructure: Cisco reported AI infrastructure orders from webscale customers exceeded $800 million in Q4 FY2025, doubling their original target.10

3. Sector Analysis: The Enterprise Adopters

3.1. Enterprise Software: The Shift to Contractual Backlog

The financial impact of AI is transitioning from theoretical potential to measurable metrics in Remaining Performance Obligations (RPO).11

Surging Backlogs: Oracle reported fiscal Q4 2025 RPO of $138 billion (up 41% YoY).12 SAP saw its cloud backlog expand 29% to €18.2 billion.

Emerging AI Revenue: Salesforce disclosed that Data Cloud and AI ARR surpassed $1 billion in Q1 fiscal 2026, growing over 120% YoY.13

Monetization via Efficiency: Meta reported a 22% revenue increase in Q2 2025, driven by AI algorithms that improved ad recommendations and increased time spent on platform by 5%.

3.2. Financial Services: Security as a Growth Engine

For global payment networks and banks, AI is central to "Value-Added Services," growing faster than core transaction volumes.

Monetizing Trust: Mastercard revealed AI enables one in three of its value-added services, driving 18% currency-neutral revenue growth in that segment.14

Wealth Management: ICBC’s "AI wealth assistant" contributed to a 24.5% YoY increase in corporate wealth management income. JPMorgan Chase highlights AI as essential for supporting its 21% Return on Tangible Common Equity (ROTCE).

3.3. Pharmaceuticals: Reducing R&D Friction

AI is shifting from a research tool to a driver of operational margin defense.

R&D Efficiency: Roche is using AI to compress clinical trial documentation timelines from months to days, maintaining flat R&D spending while refilling pipelines.

Operational Productivity: UnitedHealth Group’s Optum Insight used AI-powered claims tools to increase productivity by over 20%, expanding operating margins to 20.7%.

3.4. Retail and Industrial Application

Retail Operations: Walmart credited its "Sparky" AI assistant with driving e-commerce sales growth of 25% globally.15

Robotics: Tesla continues to increase AI operating expenses for Full Self-Driving, viewing this as a shift from hardware profits to higher-margin fleet profits.

4. Emerging Macro-Themes

4.1. The "Second Wave" of Infrastructure

While chips defined the first wave, networking and energy are the second.

Networking: Cisco reported triple-digit growth in orders from webscale customers for the fourth consecutive quarter.

Energy: Chevron announced a "giga-watt scale power solutions venture" for data centers; ExxonMobil is leveraging AI for $18 billion in structural cost savings.16

4.2. "Sovereign AI" and Localized Infrastructure

A new revenue theme is the push by nations to own AI infrastructure.

National Factories: NVIDIA and Oracle are seeing strong demand from Japan, Canada, France, and Germany for "Sovereign Clouds" distinct from public hyperscalers.

4.3. The CapEx vs. Revenue Lag

The critical narrative for late 2025 is the disconnect between immediate CapEx and long-term revenue.

The Investment Gap: While Microsoft and Google see immediate accretion, Meta and Tesla are front-loading investments (Meta raising CapEx to $37-40 billion) with a longer monetization horizon, placing pressure on ROIC metrics.

The Great Divergence of 2025

The first half of 2025 has crystallized a stark economic divergence. On one side, the "AI Industrial Complex"—comprising hyperscalers, chipmakers, and energy providers—is operating in a boom cycle characterized by historic capital expenditures and accelerating revenue. On the other side, the consumer economy is fracturing; while the aggregate consumer remains resilient, distinct cracks have appeared among lower-income demographics, forcing a pivot toward value-seeking behavior that is reshaping retail and food service.

Here are the key findings from the 1H 2025 earnings season:

1. The AI CapEx "Arms Race" and the ROI Question

The defining financial narrative of 2025 is the unprecedented capital deployment into AI infrastructure. The major cloud providers are no longer piloting AI; they are re-architecting their entire expense structures around it.

Historic Spend: Microsoft’s capital expenditures hit $21.4 billion in a single quarter (Q3 FY25), driven by cloud and AI demand that continues to outstrip supply,. Alphabet echoed this, reporting CapEx of $13.2 billion in Q2 alone, with management signaling that depreciation expenses will accelerate as technical infrastructure comes online. Meta raised its full-year CapEx guidance to a range of $37–$40 billion to support its AI roadmap.

The Hardware Windfall: NVIDIA continues to capture the lion's share of this spend, with Q2 Data Center revenue reaching $26.3 billion (reported as $41.1 billion in their fiscal Q2 2026), up 56% year-over-year. TSMC confirmed that high-performance computing (HPC) now accounts for more than half of its revenue, driving a 36% year-over-year revenue increase in Q2,.

Monetization is Real but Early: Microsoft reported that AI services contributed 7 points to Azure's growth. Amazon Web Services (AWS) is seeing an annualized revenue run rate exceeding $105 billion, fueled by customers resuming cloud migrations and adopting generative AI.

2. The Consumer: A Tale of Two Wallets

The consumer economy has bifurcated. While topline spending remains positive, the composition of that spending has shifted aggressively toward "value."

The Value Pivot: Walmart is the clear winner in this environment, delivering strong share gains across all income cohorts, particularly upper-income households trading down. They reported 4.8% revenue growth in Q2 and raised full-year guidance, driven by essentials and private brands,.

Discretionary Pressure: Conversely, Home Depot reported a 3.3% decline in comparable sales in Q2, citing "softness in larger discretionary projects" where customers typically use financing,. McDonald’s saw global comparable sales decrease by 1.0% in Q1, acknowledging that lower-income consumers are pulling back and forcing the chain to rethink its value platform,.

Experience vs. Goods: Visa and Mastercard noted that consumer spending remains resilient but is supported by a strong labor market. Cross-border travel volume remains robust (up 16% for Visa), indicating consumers are still prioritizing experiences over goods,.

3. Healthcare: The Obesity "Duopoly" and Pipeline Maturation

The pharmaceutical sector is dominated by the metabolic revolution, though supply chains and compounding pharmacies remain friction points.

Hyper-Growth in Metabolic: Eli Lilly’s Zepbound generated $1.24 billion in Q2 revenue alone, and the company raised its full-year revenue guidance by $3 billion due to strong demand. Novo Nordisk reported 18% sales growth in Q1 but slightly lowered full-year sales outlooks due to pricing dynamics and the persistence of compounded GLP-1s in the U.S. market.

Loss of Exclusivity (LOE) Management: AbbVie is successfully navigating the "patent cliff" for Humira. Despite Humira revenues falling ~30%, the company raised its full-year guidance as its replacement immunology assets, Skyrizi and Rinvoq, outperformed expectations.

4. Financial Services: Investment Banking Reawakens

After a dormant 2023–2024, capital markets activity has returned, boosting fee revenue for major banks.

Fee Revenue Rebound: JPMorgan Chase reported Investment Banking fees up 50% year-over-year in Q2. Bank of America saw investment banking fees rise 29%, signaling that corporate confidence to engage in M&A and debt issuance has returned.

Credit Quality: Despite macro noise, credit quality remains robust. Bank of America reported net charge-offs were steady at $1.5 billion, signaling that the much-feared credit cycle has not materialized.

5. Operational Efficiency as a Permanent Discipline

Across sectors, companies are maintaining "pandemic-era" efficiency disciplines even as growth returns.

Margin Expansion: Amazon achieved record operating margins in North America and International segments, attributing this to a re-architected fulfillment network that places inventory closer to customers.

Cost Discipline: Meta reported an operating margin of 38% (up from 25% the prior year), proving that its "Year of Efficiency" was a structural reset rather than a one-time event. Salesforce continues to expand margins through disciplined hiring and resource allocation.

Analyst's Take

Investors should monitor the "ROI Gap" in the second half of 2025. While tech giants are spending billions on AI infrastructure,, the market will increasingly demand evidence of revenue accretion from these investments. Furthermore, the divergence between Walmart's strength and McDonald's weakness suggests that companies perceived as offering "value" will outperform those perceived as having taken excessive pricing action over the last two years.

Methodology

Methodology: Analytical Framework for AI Economic Impact

The analysis provided utilizes a fundamental equity research framework, aggregating data from Q1 and Q2 2025 earnings reports, press releases, and management webcasts. The methodology focuses on segregating capital allocators from capital beneficiaries to determine the flow of AI-related liquidity through the economy.

1. Cohort Segmentation

The analysis bifurcates the market into two distinct economic cohorts to isolate specific financial behaviors:

Infrastructure Builders: Companies manufacturing chips or hosting models (e.g., NVIDIA, TSMC, Microsoft, Alphabet). For this group, the methodology focuses on Capital Expenditure (CapEx) growth as a leading indicator of future capacity and Data Center Revenue as a lagging indicator of current demand,,.

Enterprise Adopters: Companies in non-tech sectors (e.g., Walmart, AbbVie, JPMorgan). For this group, the methodology isolates Operating Margin and SG&A leverage to quantify the deflationary impact of AI on labor and administrative costs,,.

2. Capital Intensity vs. Monetization Lag

We analyze the disparity between current investment and realized revenue to assess the "ROI Horizon." This involves:

CapEx Tracking: Aggregating the capital expenditure guidance of hyperscalers (Microsoft, Meta, Alphabet, Amazon) to quantify the aggregate industry bet on AI infrastructure,,.

Revenue Attribution: Filtering specifically for "AI-related" revenue contributions within broader cloud segments. For example, distinguishing general Azure growth from AI-specific Azure services, or isolating "Data Center" revenue from gaming revenue for NVIDIA.

3. Qualitative Thematic Extraction

Beyond quantitative metrics, the methodology synthesizes management commentary to identify emerging commercial vehicles for AI.

Sovereign AI: We identified specific management mentions of nation-state buying patterns to validate a new customer class distinct from enterprise or consumer,.

Agentic AI: We tracked the shift in nomenclature from "generative AI" (chatbots) to "agentic AI" (autonomous action) across software providers like Salesforce and Microsoft to identify the next phase of product pricing power,.

4. Operational Efficiency Analysis

To measure the impact on the broader economy, we analyze "efficiency ratios" and headcount productivity.

Metric Focus: We examined specific disclosures regarding tasks automated or headcount avoided. For instance, citing Salesforce's ability to redeploy headcount due to AI support agents or Roche's reduction in administrative friction in clinical trials.

5. Forward-Looking Indicator Assessment

The analysis prioritizes forward-looking metrics over historical performance to determine trend sustainability.

RPO and Backlog: We utilize Remaining Performance Obligations (RPO) and backlog growth (e.g., Oracle, Microsoft) as a proxy for future revenue durability, confirming that demand is contractual rather than speculative,.

Inventory Levels: For hardware suppliers like ASML and TSMC, we analyze inventory and bookings to assess whether demand is real or a result of panic-buying/stockpiling,.

Key Findings

- 1- AI Infrastructure Supercycle – Hyperscalers and Oracle ramping capex to historic levels for AI data centers and chips.

- 2- Semiconductor Bifurcation – Advanced AI chips driving record revenues; mature nodes under pressure from weak consumer demand.

- 3- Cloud Revenue Acceleration – AWS, Google Cloud, and Azure showing double-digit growth as AI workloads boost migrations.

- 4- Consumer Spending Divide – Upper-income households trading down to Walmart; lower-income cohorts cutting discretionary/QSR spending.

- 5- GLP-1 Supply & Access Battle – Eli Lilly and Novo Nordisk dominate metabolic disease drugs amid supply constraints and payer pushback.

- 6- Financial Services Resilience – Banks report solid credit quality and fee recovery, but NII pressured by deposit costs and rate shifts.

- 7- China Macro Headwinds – Luxury, auto, and diagnostics firms hit by reforms, weak sentiment, and competition.

- 8- Digital Advertising Strength – Meta and Alphabet see robust growth from AI-driven ad targeting, especially in retail and finance. - Trade Policy Uncertainty – Tariffs and fluid trade rules cited as risks for retail and manufacturing supply chains. Would you like me to also map these findings into sector-by-sector implications (e.g., tech, consumer, pharma, finance) so you can see the broader strategic picture?

- 9- Trade Policy Uncertainty – Tariffs and fluid trade rules cited as risks for retail and manufacturing supply chains.

Conclusions

5. Conclusion: The Bifurcated Economy

The financial reports from the first half of 2025 paint a picture of a global economy bisected by Artificial Intelligence. On one side, the AI Infrastructure Builders (NVIDIA, TSMC, Hyperscalers) are experiencing a capital supercycle characterized by immense revenue growth and historic capital intensity. On the other side, the AI Adopters (Banks, Pharma, Retail) are utilizing these technologies primarily as a deflationary force—using AI to strip out costs and defend margins against a volatile macroeconomic backdrop.

For investors and analysts, the key dynamic to monitor through 2026 is the utilization rate of this infrastructure. The transition from pilot programs to profit-generating products will determine if these historic capital outlays generate the expected return on invested capital.

About the Author

Jesus Guzman is a seasoned professional in online marketing and digital strategy. With a versatile T-shaped skill set spanning SEO, PPC, and content strategy, Jesus specializes in analyzing market trends to craft comprehensive digital strategies that drive measurable business results.

How to Cite This Research

To cite this article in academic or professional publications, please use the following format:

Guzman, J. (2025). The AI Infrastructure Supercycle: Driving Revenue Acceleration and Capital Intensity. FN Pulse. Available at: [URL]

Citations

- Alphabet Inc.

- Amazon.com, Inc. (NASDAQ: AMZN)

- ORACLE

- NVIDIA

References

- Alphabet Announces Second Quarter 2025 Results - Investor Relations team (205)https://s206.q4cdn.com/479360582/files/doc_financials/2025/q2/2025q2-alphabet-earnings-release.pdf

- AMAZON.COM ANNOUNCES SECOND QUARTER RESULTS - Amazon Investor Relations (2025)https://ir.aboutamazon.com/news-release/news-release-details/2025/Amazon-com-Announces-Second-Quarter-Results/default.aspx

- Q2 2025 Oracle Earnings - Oracle (2025)https://investor.oracle.com/investor-news/news-details/2025/Oracle-Announces-Fiscal-Year-2026-First-Quarter-Financial-Results/default.aspx

- Q1 2025 NVIDIA Webcast (1Q FY026) - Sarah (2025)https://events.q4inc.com/attendee/988346217