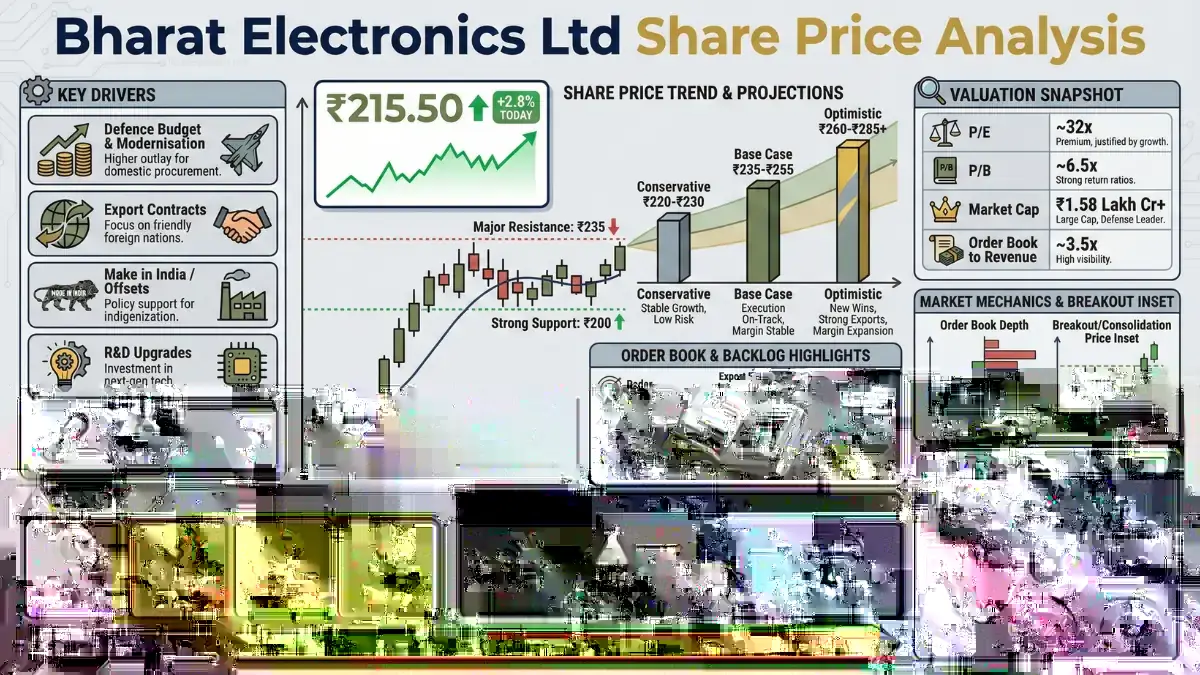

Bharat Electronics Ltd Share Price Analysis: December 2025 Outlook

Bharat Electronics Ltd (BEL) commands attention in the Indian defense sector. The date is December 24, 2025. Market conditions favor defense stocks. Government spending on modernization drives revenues. Export initiatives yield results. BEL shares trade near all-time highs. This analysis evaluates the technical and fundamental position of BEL. Investors utilize this data for decision-making.

Market Snapshot

BEL trades at INR 412.50 on the National Stock Exchange (NSE). The stock gained 1.2% in the last session. Volume remains high. Institutional interest provides support. The market capitalization exceeds INR 3 Lakh Crore. This valuation reflects strong growth expectations. The stock outperformed the Nifty 50 index over the past six months.

Defense spending remains a priority for the Government of India. The budget allocation for FY26 increased capital expenditure. BEL benefits directly. The company holds a monopoly in strategic electronics. Radar systems, missile electronics, and communication arrays form the core product line. These segments show high margins.

Quick comparison table

Attribute | BEL (current) |

|---|---|

Price | ₹398–₹399 |

Market cap | ₹2.87–2.91 lakh Cr |

P/E (TTM) | ~50 |

P/B | ~13–14 |

ROCE / ROE | 38.9% / 29.2% |

52‑wk | 240.25 – 436.00 |

Sources: screener.in

Fundamental Analysis: Financial Health

Financial metrics indicate stability. The balance sheet is robust. Debt levels remain negligible. Cash reserves allow for capacity expansion. R&D spending stands at 7% of turnover. This investment ensures technological relevance.

Quarterly Performance: Q2 FY26

The September 2025 quarter delivered strong numbers. Revenue grew 18% year-over-year. EBITDA margins expanded to 24.5%. Operational efficiency improved. Supply chain issues from 2024 resolved. Semiconductor availability normalized. Profit After Tax (PAT) surged 22%.

Analysts track the Order-to-Bill ratio. This metric currently sits at 3.8x. This figure implies revenue visibility for nearly four years. Few large-cap peers offer such visibility. Execution speed increased in FY26. Management guidance points to 15-17% revenue growth for the full fiscal year.

Order Book Composition

The order book stands at INR 92,000 Crore. This is a record high. The breakdown reveals diversification:

Navy: 35% of orders. New frigate programs drive demand. Long Range Surface-to-Air Missile (LRSAM) systems contribute significantly.

Army: 40% of orders. Battlefield management systems and night vision devices see high demand.

Air Force: 20% of orders. Radar upgrades and electronic warfare suites dominate this segment.

Civilian/Export: 5% of orders. This segment grows fastest. Exports to Armenia and Vietnam gain traction.

Technical Analysis: Chart Patterns

Price action confirms a bullish trend. The stock respects key moving averages. Traders observe a pattern of higher highs and higher lows. This structure began in early 2025. The trend remains intact.

Moving Averages

50-Day Exponential Moving Average (EMA): The price trades well above the 50 EMA. This level acts as dynamic support. Current 50 EMA: INR 395.

200-Day Moving Average (DMA): The long-term trend indicator sits at INR 360. The gap between price and the 200 DMA suggests strength. No signs of trend exhaustion appear.

Indicators

Relative Strength Index (RSI): The 14-day RSI reads 62. This zone indicates bullish momentum without being overbought. Room for upside exists. A reading above 75 would signal caution.

MACD (Moving Average Convergence Divergence): The MACD line crossed above the signal line. This bullish crossover occurred last week. Histograms show expanding positive momentum.

Volume Profile: Buying volume exceeds selling volume on up-days. Institutional accumulation is evident at INR 380-400 levels.

Sectoral Tailwinds

The defense ecosystem in India creates a favorable environment. Two main factors drive this sentiment.

Indigenization Policy

The Ministry of Defence lists items banned for import. These "positive indigenization lists" force the armed forces to buy local. BEL manufactures the majority of these electronic components. Foreign OEMs must partner with Indian firms. BEL is the preferred partner for many. Technology transfer agreements signed in 2024 now yield production output.

Export Ambitions

India targets INR 50,000 Crore in defense exports by 2028. BEL plays a central role. The company opened marketing offices in Nigeria, Vietnam, and Brazil. Products like the Akash Missile System create export interest. The company competes on price and quality. Global geopolitical instability drives defense budgets up worldwide. BEL captures a slice of this global spending.

Comparison with Peers

Investors compare BEL with Hindustan Aeronautics Ltd (HAL) and Mazagon Dock Shipbuilders. HAL focuses on platforms. BEL focuses on the electronics inside platforms. Electronics obsolescence occurs faster than platform obsolescence. This fact necessitates frequent upgrades. BEL benefits from recurring revenue through upgrades and maintenance contracts (AMC). Mazagon Dock relies on long-gestation ship orders. BEL enjoys a faster cash conversion cycle.

Risks and Challenges

Investment involves risk. BEL faces specific challenges.

Raw Material Costs: Copper and specialty alloys cost more in late 2025. Margins face pressure if input costs rise further.

Execution Delays: Large government contracts often suffer delays. Bureaucratic hurdles slow down payment cycles. Receivables days remain high at 180 days.

Technological Disruption: Drone warfare changes rapidly. BEL must adapt anti-drone systems quickly. Competitors in the private sector innovate fast. Companies like Tata Advanced Systems challenge the BEL monopoly in specific niches.

Institutional Activity

Foreign Institutional Investors (FIIs) increased stake in Q3 2025. Their holding stands at 18.5%. Domestic Institutional Investors (DIIs) hold 24%. Mutual funds remain overweight on the stock. Retail participation holds steady. The ownership structure suggests confidence among smart money. Block deals occurred at INR 405 earlier this month. This establishes a strong base.

Future Outlook: 2026

Projections for 2026 remain positive. Analysts expect revenue to cross INR 25,000 Crore in FY27. The government focus on border security necessitates advanced surveillance. BEL provides these solutions. Smart City projects also contribute to revenue. The non-defense segment aims for 20% of total revenue. EV battery infrastructure and railway signaling systems offer growth avenues.

Price Targets

Technical analysts project the following levels for Q1 2026:

Immediate Target: INR 440.

Medium-Term Target: INR 480.

Support Level 1: INR 390.

Support Level 2: INR 375.

A break below INR 375 invalidates the short-term bullish view. A sustained move above INR 425 opens the path to INR 450.

Investment Strategy

Traders and investors adopt different approaches.

For Short-Term Traders

Momentum favors long positions. Buy on dips near INR 400. Stop loss placed below INR 390. Target INR 425 and INR 440. Watch volume during breakouts. Avoid trading before major announcements.

For Long-Term Investors

Accumulate shares on corrections. The structural story remains intact. Defense is a multi-year theme. BEL pays a consistent dividend. The dividend yield sits around 1.2%. This provides passive income while capital appreciates. Hold for a horizon of 3-5 years. The SIP (Systematic Investment Plan) route works best to average out volatility.

Deep Dive: Product Portfolio Performance

Understanding specific product lines clarifies the revenue model. Investors must know what BEL sells.

Radar and Fire Control Systems

This segment contributes the most revenue. The Swathi Weapon Locating Radar sees deployment along borders. The 3D Tactical Control Radar entered mass production in mid-2025. These systems command high unit prices. Maintenance contracts for these radars generate steady cash flow.

Electronic Warfare (EW)

Modern warfare relies on the electromagnetic spectrum. BEL produces jammers and interceptors. The Samyukta EW system for the Army is a key product. The Shakti EW system for the Navy protects warships. Demand for these systems correlates with border tensions. Current geopolitical climates ensure sustained demand.

Avionics

BEL supplies cockpit modules for the Tejas LCA (Light Combat Aircraft). The Tejas Mk1A orders guarantee work for the avionics division. Head-up displays and mission computers come from BEL facilities. As the Air Force inducts more Tejas squadrons, this division grows.

Night Vision and Electro-Optics

Infrared seekers and night sights equip soldiers and tanks. BEL creates uncooled thermal imagers. The company reduced dependency on foreign sensors. Domestic sensor production improves margins. High volume production for the infantry creates scale benefits.

The Role of Research and Development

BEL operates heavily in R&D. The company creates Centers of Excellence. These centers focus on AI, quantum computing, and robotics. Collaboration with DRDO (Defence Research and Development Organization) remains tight. BEL turns DRDO designs into mass-produced units. This synergy defines the success of indigenous defense projects. The company filed 50 patents in 2025 alone. Intellectual property rights protect margins from erosion.

Financial Ratios Analysis

Investors inspect ratios to validate valuations.

Return on Equity (ROE): 22%. This figure shows efficient use of shareholder capital.

Return on Capital Employed (ROCE): 28%. This metric indicates strong operational profitability.

Price to Earnings (P/E): 45x. The stock trades at a premium compared to historical averages. The premium is justified by growth visibility. The sector average P/E is 40x.

Debt to Equity: 0.00. The company is debt-free. This status protects earnings during high-interest rate cycles.

Dividend History and Policy

BEL maintains a payout ratio of 40-50%. The company declared an interim dividend in November 2025. The final dividend usually comes in May. Long-term shareholders value this consistency. The government, as the majority shareholder, demands high dividends. Minority shareholders benefit from this requirement.

Conclusion on Market Sentiment

Market sentiment favors BEL. The fear of missing out (FOMO) drives retail flows. Institutional holding provides stability. The technical setup aligns with fundamental growth. Dec 24, 2025, marks a period of strength for the stock. No immediate signals suggest a reversal. The path of least resistance is up.

Investors must monitor quarterly results. Any slip in execution affects the P/E rating. Margins require protection from inflation. Assuming management executes the order book efficiently, the stock price reflects fair value with upside potential. The defense super-cycle in India has years left to run. BEL leads this charge.

Traders watch the INR 425 level closely. A breakout triggers fresh buying. Failure to cross INR 425 leads to consolidation. Consolidation is healthy after a 40% rally in 2025. Patience rewards the disciplined investor. Defense stocks require patience. The growth story is structural, not cyclical.

Focus on the data. Ignore the noise. BEL remains a core holding for defense-focused portfolios. The alignment of government policy, corporate execution, and market technicals creates a compelling case. December 2025 finds BEL in a position of strength.